BRRRR Bookkeeping: How to Track a Refinance-Out Without Losing Your Cost Basis

You bought the duplex on Liberty Street back in March. You financed the rehab on a HELOC and a credit card you swore you would pay off the moment cash came back. You closed the cash-out refi in October. Now your CPA wants a number for cost basis, and you are staring at a QuickBooks file that lumped the HELOC draws, the credit card payments, the contractor checks, and the refi proceeds into one moving target. You do not know what your basis is. You do not know what your equity is. You do not know what the refi actually freed up versus what is still a borrowed dollar moving around inside the system.

If that paragraph describes you, you are not alone. BRRRR - Buy, Rehab, Rent, Refinance, Repeat, is one of the cleanest wealth-building strategies in residential real estate. It is also one of the easiest to lose track of on the books, because every single cycle has at least three financing events and two valuation events compressed into six to twelve months. Buy-and-hold books drift. BRRRR books accelerate.

This is a Hampton Roads question too. In Norfolk, Portsmouth, Hampton, and the older parts of Chesapeake, BRRRR is one of the most active strategies among investors I work with — because the housing stock has the right age, the right entry prices, and the right rent-to-value ratios for the model to work. Which means the bookkeeping question is not theoretical. It is something you need answered before the next refi.

Why BRRRR is Harder on Books Than Buy-and-Hold

Buy-and-hold has two financial events per property in a normal year. The purchase. Operating activity. That is it. The accounting framework is steady. Income, expenses, depreciation, end of story.

BRRRR has at least five in the first twelve months. Purchase. Rehab funding, often layered across cash, HELOC, hard money, credit card, and contractor financing. Rehab spending, split between repairs and capital improvements, which matters enormously for taxes. Lease-up. Refinance.

Each of those events affects basis, equity, depreciation, and the loan-to-cost ratio that the next lender will want to see. Every dollar has a job. If the books cannot tell the story of that dollar, you cannot prove what the next refi is actually doing.

What Has to Be Tracked on Every BRRRR Cycle

There are five things investor-grade BRRRR books need to capture per property, every cycle. Most of the QuickBooks files I see capture two or three of them.

The purchase price, broken into land and building. This sets your depreciation base and your starting cost basis. If your books only track the closing as a single number, you have a problem the day the depreciation schedule needs to be built.

Rehab spending, separated into repairs and improvements. Repairs go to the current-year operating line. Improvements get capitalized into cost basis. This is not optional and it is not a small distinction. A new HVAC system is a capital improvement. A repair to the same HVAC system three months after install is a repair. One adds to basis. The other does not.

Every source of rehab financing, tracked separately. HELOC, credit card, hard money, owner cash, contractor financing, each is a different liability with a different interest treatment. When the refi pays them off, the books have to show which liability each refi dollar retired.

The refinance event itself. The new loan amount. The payoff of the construction debt. The cash returned to the investor, if any. The closing costs, which capitalize rather than expense. The new equity position.

Post-refi operating activity. Rents, expenses, depreciation on the new basis, and the new monthly debt service. This is the part most investors get right. It is what is happening below the surface that gets missed.

The Refi-Out Step is Where Most Investors Lose Their Cost Basis

This is the part I want you to read twice.

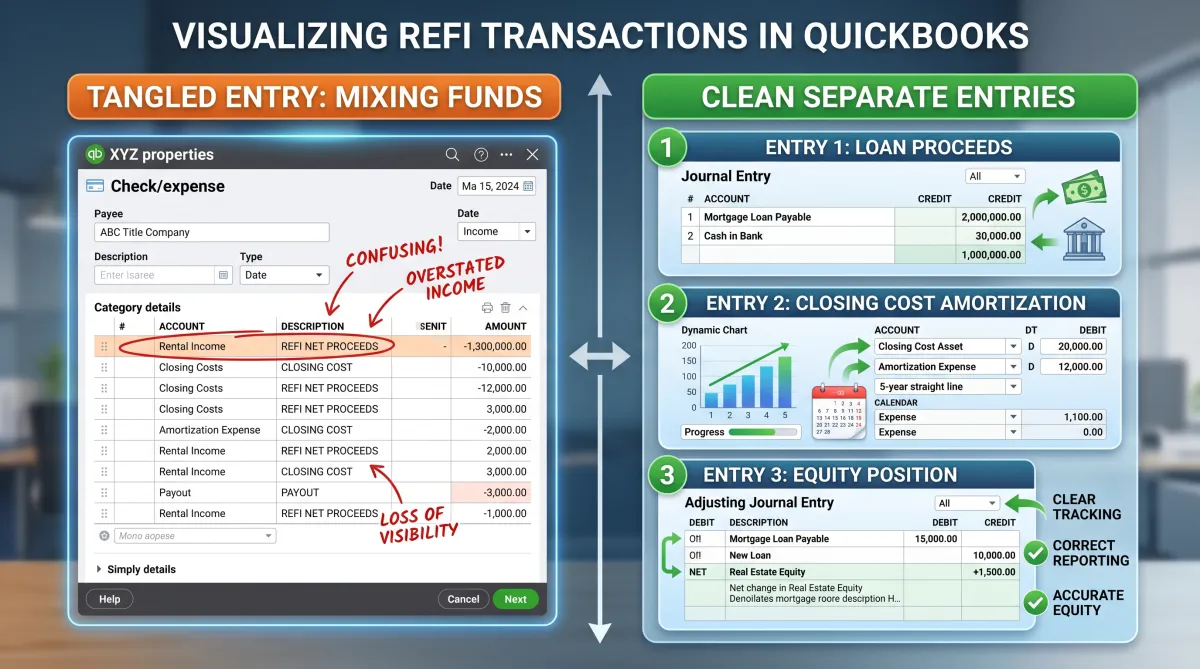

When you cash-out refinance, two things happen in the books that confuse almost everyone. The new mortgage is a new liability, that part most people get. But the refi proceeds are not income. They are not a contribution to the LLC. They are debt that arrived as cash. If you book them as income, you owe tax on dollars you never earned. If you book them as a member contribution, your equity rolls off the rails. They are loan proceeds. That is the only correct treatment.

The second thing is what most BRRRR investors miss entirely. The closing costs on the refi — title, lender fees, points, recording fees do not get expensed in the year of the refi. They amortize over the life of the new loan. Twenty-five hundred dollars in lender fees on a thirty-year refi expenses at roughly eighty-three dollars a year. Not all at once. The IRS is specific about this and so is the lender on the next deal who is going to look at your debt-service-coverage ratio.

If your books capitalized those costs incorrectly, either by expensing all of them in the refi year or by ignoring them entirely, your operating margin will look wrong, your tax return will be wrong, and the next refinance lender will be reading a financial statement that does not reflect what really happened.

Hampton Roads BRRRR, A Quick Note on Local Factors

If you are running BRRRR cycles here specifically, there are a few local realities worth noting at the books level.

Property tax rates vary by jurisdiction. Norfolk, Chesapeake, Virginia Beach, Portsmouth, Suffolk, Hampton, and Newport News are all different rates, and several have supplemental special-purpose taxes for specific neighborhoods. Your books should track property tax by city, not as a single lump.

Many of the older Norfolk and Portsmouth neighborhoods where BRRRR works best have insurance underwriting quirks tied to flood zones and home age. The insurance line on those properties can move twenty to forty percent year over year. Track it by property, not as a portfolio average.

Property managers in Hampton Roads who serve smaller investors often consolidate multiple properties on a single monthly statement. If your books accept that statement as one entry, you have lost per-property clarity. The fix is a reconciliation discipline, every PM statement gets unbundled before it touches QuickBooks.

What Refinance-Ready BRRRR Books Look Like

When a lender pulls financials for the next refinance, here is what they want to see and what your books should produce inside five minutes:

A per-property profit and loss for the trailing twelve months.

A current balance sheet showing each property's basis, accumulated depreciation, mortgage balance, and equity position.

A schedule of capital improvements made since purchase, dated and categorized.

A clean separation between operating activity and financing activity.

Owner equity tracked separately from the LLC's retained earnings.

If your books cannot produce that in five minutes, the lender is going to assume the property is more risk than the numbers say it is. You may still get the refi, but you may get a worse rate, a lower LTV, or a longer underwriting cycle. All three cost real money on a BRRRR strategy that depends on velocity.

When to Bring This Outside

You can run BRRRR books in-house if you are running one cycle a year and you have the time and the patience. Most investors I meet who are running two or more cycles a year or who have started layering LLCs to protect different properties from each other, have hit the point where the bookkeeping is consuming hours that should be going into the next deal.

That is the conversation worth having. Not "should I outsource bookkeeping" as a yes-or-no question, but "what is the cost of every hour I spend on this versus on the next acquisition." For most of the BRRRR investors I work with, the answer becomes clear inside one quarter.

If you are running BRRRR cycles in Hampton Roads and your books are not producing refinance-ready financials on demand, that is a conversation worth having. Book a call with Hines Bookkeeping and we will look at where your current setup is bleeding clarity and what investor-grade BRRRR books would look like for your portfolio.